Bank Loans: The Missing Piece

- May 6

- 7 min read

Updated: May 7

If you had the potential opportunity to increase returns while reducing risk, wouldn’t you take it?

For investors seeking a steady, income-generating investment that has historically shown far less volatility than other fixed income alternatives, bank loans—also known as leveraged, floating rate and broadly syndicated loans—might be the solution. The asset class has been a dependable source of income and return for investors for decades, delivering attractive performance across a variety of market conditions.

Yet, in conversations with allocators, we continue to observe that the asset class is under-owned, as fewer investors hold loans in a dedicated manner versus high yield and investment grade bonds. We would argue that bank loans are “the missing piece” for many portfolios, as shown by their historical ability to generate attractive, consistent total returns—primarily from income—while at the same time offering the benefit of reducing overall portfolio volatility.

Key Potential Benefits of Bank Loans:

Consistent Income: Returns are generated primarily from contractual coupon payments, providing a reliable income stream

Lower Interest Rate Risk: The floating-rate structure can minimize the impact of interest rate fluctuations, offering a more direct exposure to corporate credit compared to fixed-rated bonds, which are subject to duration risk

Senior Secured Status: Bank loans are primarily backed by a legal claim (lien) on company assets, offering greater protection in the event of default and priority of payment, resulting in average higher recoveries versus unsecured debt

Diversification Benefits: Bank loans have historically demonstrated low correlation to equities and traditional fixed-income assets, helping to reduce overall portfolio volatility and enhance risk-adjusted returns

What Are Bank Loans?

Bank loans are senior secured, typically first-lien debt issued by companies with below-investment-grade credit ratings. Unlike traditional bonds, bank loans typically have a floating-rate coupon that adjusts (usually quarterly) based on a benchmark rate, such as the Secured Overnight Financing Rate (SOFR), paying investors a spread above this base rate.

The bank loan market has existed for decades, growing from a nascent asset class in the early 90s—with the inception of the S&P UBS Leveraged Loan Index dating back to January 1992—to a $1.6 trillion market in 2025, now larger than even the high yield bond universe. As a team, Artisan Credit has been actively investing in loans for over a decade, successfully deploying more than $15 billion of capital on behalf of our investors.

A Track Record of Reliability

While the asset class has evolved over time, one of its most notable characteristics—consistency of historical returns—has not changed. Investors in bank loans derive their returns primarily from coupon income while their floating rate nature can limit the interest rate risk found in longer duration assets. The combination of these two traits has enabled investors to earn attractive total returns that are typically more insulated from interest rate volatility than fixed rate assets, such as high yield and investment grade bonds. In effect, we believe bank loans can offer investors one of the purest forms of corporate credit exposure.

To illustrate the consistency of the asset class, we examined historical returns for the S&P UBS Leveraged Loan Index across a variety of time periods and frequencies. In the 34 calendar years of its existence, which have included a number of interest rate cycles, the loan index generated positive returns in 31 of them—more than 91% of the time. In addition, in two of the three negative calendar years (2015, 2022), the loan index achieved significant outperformance versus the high yield bond market (as measured by the ICE BofA US High Yield Index), while the index performed similarly to high yield in the third instance (2008).

When reviewing monthly periods, the differences between loans and other fixed income sectors are even more pronounced. Since inception, the loan index has posted positive returns in approximately 83% of months while investment grade bonds have recorded positive returns in only 65% of months in the same period (as measured by the ICE BofA US Broad Market Index, an aggregate bond index).

If investors are looking for the “missing piece” in their portfolios, we think a

dedicated allocation to bank loans is a worthy contender.

Why Bank Loans Are an Attractive Alternative

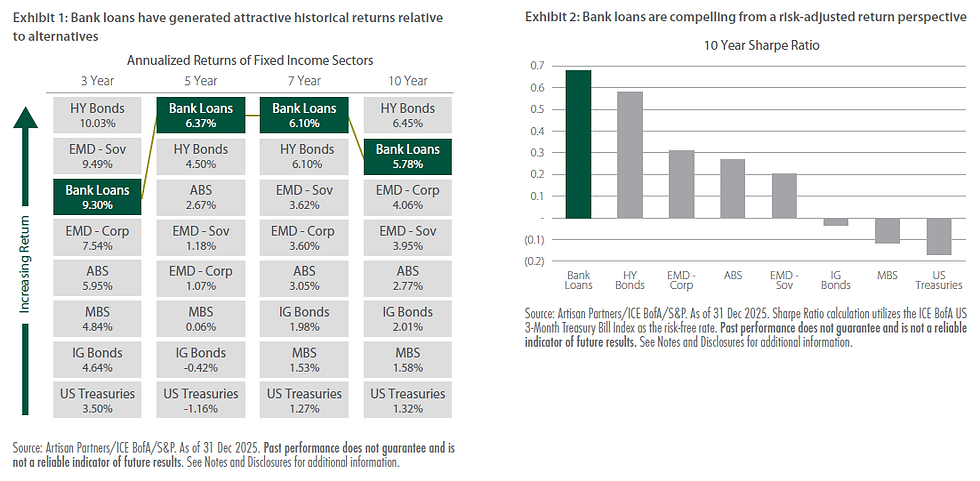

Given that most investors typically rely on fixed income assets to generate consistent returns over the long term, empirical data suggests the loan market has done a better job than investment grade bonds—the asset class typically chosen to fulfill this role.

Bank loans have delivered strong total returns compared to other fixed income assets across various timeframes—three, five, seven, ten years, and beyond. The strong performance of the asset class is particularly notable on a five- and seven-year basis, with significant outperformance in periods that include the tariff-induced market selloff of 2025, the inflation and rate shock of 2022 and the COVID recession of 2020 (for the seven-year comparison). However, in our view this performance is even more impressive when adjusted for risk (volatility). Bank loans have historically demonstrated less volatility, meaning their returns have been more stable and more consistent than other fixed income options. The end result is that, over the past ten years, bank loans have exhibited superior efficiency (as measured by Sharpe Ratio) when compared to most traditional fixed income sectors. The Sharpe Ratio is a simple way to measure how much return an investment provides for the risk taken, providing a gauge of efficiency for an asset. A higher Sharpe Ratio means that investors receive better returns for each unit of risk, making bank loans an attractive choice among fixed income alternatives for balancing both return and stability.

In addition, bank loans have relatively low correlation to other segments of fixed income by virtue of their floating rate and shorter duration nature. Over the 34-year history of the loan index, the asset class exhibited low—if not outright negative—monthly return correlation to many assets, providing valuable portfolio diversification benefits.

To highlight the aggregate potential benefits of the asset class, we examined how a traditional 60% equity and 40% fixed income portfolio performed over a five- and ten-year period when replacing the entirety of the fixed income portfolio (investment grade bonds) with leveraged loans. As illustrated below, on a five-year basis, the addition of bank loans increased returns and reduced risk leading to a substantial improvement in portfolio efficiency. Over the ten-year period, loans improved performance without materially increasing risk—resulting in a better overall Sharpe Ratio for the investor.

We recognize that replacing investment grade bonds or other longer-duration fixed income assets entirely is impractical for most investors. Instead, allocators can strategically adjust their fixed income holdings to align with their objectives. The good news is that even a modest allocation to loans may meaningfully improve portfolio outcomes.

When reviewing a two-asset efficient frontier over the 34-year history of the loan index (below), the advantage of loans is clear—pairing loans with a traditional investment grade bond allocation has materially reduced volatility while significantly enhancing returns. For example, a portfolio allocated 50% to investment grade bonds and 50% to bank loans achieved an annualized total return more than 50 bps higher than a portfolio invested solely in investment grade bonds—with lower volatility. On a $10,000 initial investment, the annual incremental return translates to an additional gain of more than $9,000 over the period, while the inclusion of loans also stabilized returns by lowering overall portfolio fluctuations.

Looking Forward

While we have focused much of our discussion on the historical performance of the asset class, we believe it’s worth highlighting the potential benefits that loans could offer on a forward-looking basis. The chart below shows that leveraged loans currently offer some of the highest yields across the fixed income landscape. This is particularly notable when comparing leveraged loans versus investment grade bonds, but even when measured against other higher yielding sectors—such as high yield bonds and emerging market debt—loans offer greater total return potential. It’s worth noting that in absolute terms, loan yields today are attractive relative to recent history, as the index level yield hit an all-time low of 4.7% in mid-2021.

From a risk adjusted perspective, we believe the loan asset class also shines bright. Given their low interest rate sensitivity (duration), loans have been the most efficient asset in the group, offering by far the most yield per year of duration. Importantly, the yield quoted for bank loans is reflective of current market expectations of the forward path of interest rates.

Finally, we believe bank loans can offer compelling returns across a variety of interest rate scenarios. If treasury yields rise materially from current levels, the low interest rate duration of loans may allow them to outperform virtually all fixed rate assets, who typically exhibit a much higher degree of sensitivity to changes in interest rates. However, even in a stable or declining rate environment, bank loans can produce compelling total returns aided by attractive absolute yields.

Conclusion

We are not alone in recognizing the power of loans within a diversified investor’s portfolio. In Morningstar’s 2023 article “How to Invest Better With Bonds”, they concluded that “leveraged loans may deserve a greater role in many portfolios”. We wholeheartedly agree, as we have shown that the asset class has historically offered a rare combination of consistency, attractive total returns and compelling diversification benefits. If investors are looking for the “missing piece” in their portfolios, we think a dedicated allocation to bank loans is a worthy contender.

To view as a PDF, click here.

This information has been prepared by Artisan Partners for Copia Investment Partners Limited (AFSL 229316, ABN 22 092 872 056) the issuer, distributor and responsible entity of the Artisan Credit Opportunities Fund. This document provides information to help investors and their advisers assess the merits of investing in financial products. We strongly advise investors and their advisers to read information memoranda and product disclosure statements carefully and seek advice from qualified professionals where necessary. The information in this document does not constitute personal advice and does not take into account your personal objectives, financial situation or needs. It is therefore important that if you are considering investing in any financial products and services referred to in this document, you determine whether the relevant investment is suitable for your objectives, financial situation or needs. You should also consider seeking independent advice, particularly on taxation, retirement planning and investment risk tolerance from a suitably qualified professional before making an investment decision. Neither Copia Investment Partners Limited, nor any of our associates, guarantee or underwrite the success of any investments, the achievement of investment objectives, the payment of particular rates of return on investments or the repayment of capital. Copia Investment Partners Limited publishes information on the document that is, to the best of its knowledge, current at the time and Copia is not liable for any direct or indirect losses attributable to omissions from the document, information being out of date, inaccurate, incomplete or deficient in any other way. Investors and their advisers should make their own enquiries before making investment decisions. © 2026 Copia Investment Partners Ltd.

Comments